Flexible spending accounts (FSAs) and health savings accounts (HSAs) are both popular options designed to help individuals manage and reduce out-of-pocket healthcare expenses. While they share the goal of making healthcare more affordable, their mechanisms, benefits, and limitations differ significantly. This article delves into these differences with a focus on providing practical insights for consumers and employers.

Understanding Flexible Spending Accounts (FSAs)

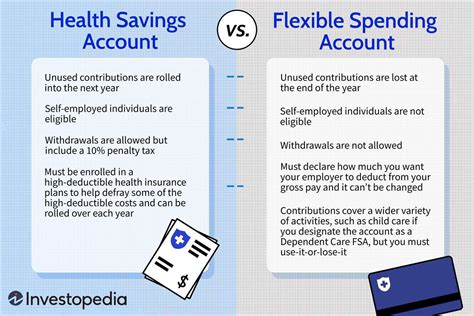

Flexible spending accounts are employer-sponsored programs that allow employees to set aside pre-tax money from their paycheck to pay for eligible medical expenses. The funds are typically used for a wide range of healthcare costs, including co-payments, deductibles, and certain over-the-counter medications. Unlike other savings vehicles, FSAs come with a “use-it-or-lose-it” provision. This means that any unspent funds generally cannot be carried over to the next year, which can be a drawback for some individuals.Exploring Health Savings Accounts (HSAs)

Health savings accounts are tax-advantaged accounts available to individuals enrolled in high-deductible health plans (HDHPs). HSAs allow contributions to be made on a pre-tax basis, and the funds can be used to pay for qualified medical expenses. Unlike FSAs, HSA funds can roll over from year to year and grow tax-deferred, providing significant long-term savings potential. Moreover, after reaching a certain age, HSA funds can be used for any expense, not just medical ones, offering a valuable retirement savings vehicle.Key Insights

- FSAs provide immediate relief from healthcare costs but have a use-it-or-lose-it rule.

- HSAs offer long-term savings potential and flexible spending for qualified medical expenses.

- HSA funds can be rolled over year to year, and can be used for any purpose after the account holder turns 65.

Choosing between an FSA and an HSA requires careful consideration of individual healthcare needs, financial goals, and the structure of the employer's plan.

Which is more beneficial, FSA or HSA?

The choice between an FSA and an HSA depends on individual circumstances. If you anticipate significant, short-term medical expenses and don't mind losing unspent funds, an FSA may be beneficial. Conversely, if you're looking for long-term savings and can meet the eligibility for an HDHP, an HSA offers substantial advantages, including tax-deferred growth and flexibility in withdrawals.

Understanding the specifics of these accounts can help individuals make informed decisions about their healthcare financing options.

While both flexible spending accounts and health savings accounts aim to make healthcare more affordable, their distinct features mean different benefits for different individuals. FSAs offer immediate relief from healthcare expenses, but their lack of carryover capability can be a significant drawback. In contrast, HSAs provide a robust long-term financial strategy, offering flexibility and tax advantages that can accumulate over time. By evaluating personal healthcare patterns and financial goals, individuals can choose the most suitable option to optimize their healthcare expenditure management.